By: Liz Strait, PhD

Introduction

In its latest Global Wealth Management Report, EY focused on two main, and perhaps related, issues: increasing complexity and escalating market volatility. According to the report, 40% of individuals believe that wealth management has become more complex in the last two years, and 57% feel financially insecure because of market volatility.

In the face of economic instability specifically, the report stresses the importance of viewing clients through a behavioral lens. This means recognizing and prioritizing psychological factors in financial decision-making. Measuring behavioral characteristics and blind spots can provide Financial Professionals (FPs) with insights into their clients’ decision-making styles, preferences, and main motivators that are inaccessible through more traditional segmentation models.

Research from Envestnet, also finds that in the face of volatility and uncertainty, people in general prefer more human-to-human interaction in the provision of financial advice. This highlights the importance of the intersection between digital and human—clients, particularly younger ones, want personalization facilitated by technology (i.e., behavioral insights, AI-powered recommendations, and data-driven decision-making) with the individual connection and support provided by a well-informed FP.

While a large body of research and empirical evidence supports all generational members feeling overwhelmed by complexity, uncertainty, and volatility, there are major similarities that should be underscored. The most important of these similarities is that members of all generations want to engage with a human FP to some extent. There is anecdotal evidence, or perhaps just mistaken stereotypes, that younger generations (Millennials and Gen Z) would prefer all-digital interfaces if possible. However, this is simply not true. In fact, Envestnet found that for younger generations, while digital is important, they still desire the human connection afforded by an FP.

For younger generations, while digital is important, they still desire the human connection afforded by a Financial Professional.

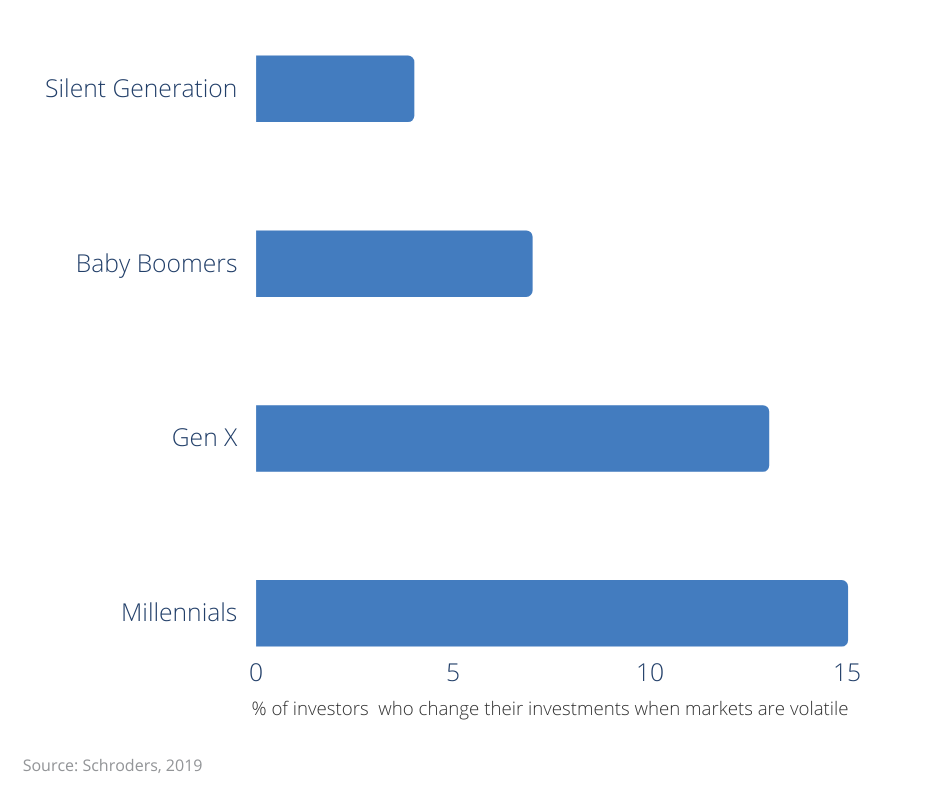

While there are similarities in terms of preferences around financial advice and guidance, there are distinct differences across generations in terms of their responses to uncertainty and instability. And these responses, while requiring more nuanced insights, highlight the importance of the intersection of digital personalization and human connection once again.

Consider this finding from EY: Millennials, compared to Boomers and Gen X, are the most likely to respond to market volatility by shifting more of their investments to savings and deposits. While this fact is reported, speculation as to why is not. So, what motivators and blind spots could be leading to this suboptimal response by Millennials?