By: Liz Strait, PhD

Ahead of our Spotlight call on June 21st at 4pm ET focusing on how men and women differ in terms of financial decision-making and outcomes, we discuss gender differences in financial literacy. Financial literacy has been linked to positive financial behaviors and outcomes, including preparation for retirement, savings levels, and credit scores. This highlights the importance of understanding key individual differences in financial literacy.

Introduction

Financial literacy is a form of consumer expertise and skill. It measures how well an individual understands important financial concepts, as well as their ability to manage their own finances. This management means that people are expected to conduct both short- and long-term financial planning while integrating ever-changing market conditions and major life changes.

Both men and women would greatly benefit from the use of an Financial Professional, albeit for different reasons and in different ways.

As with many skills, there is a large degree of variance across the population. While this variance exists at all stratifications of society (i.e., age, socioeconomic status), there are significant differences by gender that have been identified across 25 years of research. These differences between men and women are not highlighted to conclude one gender is superior to the other or to presuppose biological differences as the cause, given all differences presented will pertain to observable outcomes, not evolutionary processes. It is also important to keep in mind that all these conclusions are based on aggregate analyses—no single person will necessarily conform to all of these findings, but men and women will, on average, show these differences.

His and Hers

Spoiler alert: women have been found to be consistently less financially literate than men.1 This is not because they are incapable or lack the ability to learn financial literacy skills, but rather because of gender norms and expectations around who handles household finances (in terms of investing and allocating money, not paying bills and tracking balances).2 Financial illiteracy has been tied to several negative outcomes: increased levels of debt3, lower credit scores4, less savings5, a lower propensity to invest in the stock market6, and less wealth accumulation.7 This means women are increasingly vulnerable to financial hardship8 and experience significantly greater financial distress9, general stress, and financial anxiety.10

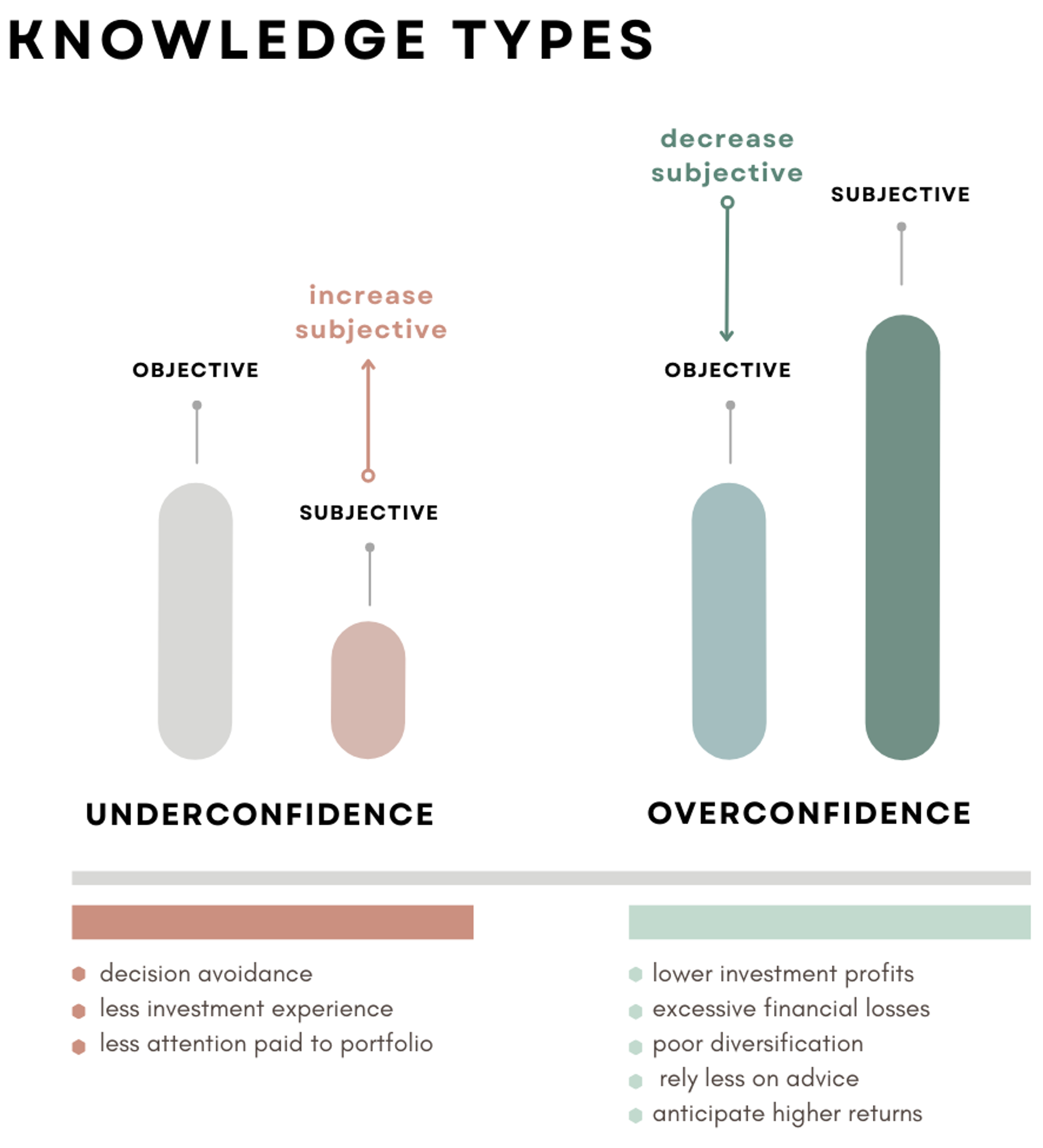

Much of the difference in financial literacy between men and women has to do with confidence in financial knowledge and ability. There is a distinction between what is called objective knowledge (what we actually know about a topic) and subjective knowledge (what we think we know about a topic). These two things do not have to be, and rarely are, the same. In fact, most researchers consider these forms of knowledge as distinct (i.e., uncorrelated and attributable to distinct underlying factors). Interestingly, women’s perception of their financial knowledge (that is, subjective knowledge), is 1.6 rating points, or 32%, lower than men’s, despite objective knowledge being unaffected by gender.11

So, what happens when you have an imbalance between objective and subjective knowledge? When subjective knowledge is greater than objective knowledge, a person is overconfident; when subjective knowledge is less than objective knowledge, a person is underconfident. This means men are more likely to be overconfident and women are more likely to be underconfident when it comes to financial decision-making. While both under- and overconfidence can result in clients neglecting or incompletely processing new information, overconfidence is far worse for a client’s financial decision-making.12 Overconfidence results in lower levels of investment profits13, excessive financial losses14, and poor diversification.15 Of special significance to Financial Professionals (FPs), overconfidence results in a client relying less on their FPs’ advice, believing returns are highly predictable, and anticipating higher potential returns.16

Underconfidence is not without its own negative consequences—it can result in financial decision avoidance17, less investment experience18, and less attention paid to one’s portfolio.19 Some of the underconfidence found in women is attributable to the finding that women believe they make decisions more emotionally, but that financial matters need to be assessed analytically and in a manner devoid of emotion.20 It is this mismatch that can lead to underconfidence and avoidance. What is perhaps most interesting about this finding is that while many women believe they make decisions more emotionally, they, in fact, tend to be significantly more analytical in their decision approach than men.21 The cause of this discrepancy between beliefs and reality is likely borne of the stereotype that women are more emotional. In fact, research has shown that when it comes to the likelihood of investing, men are more influenced by their emotions22 than women.23

Ultimately, differences in financial literacy between men and women are not the result of superior skills or ability, but rather psychological processes, deeply ingrained social norms, and sex-based stereotypes. This suggests that FPs can have a significant impact in helping with financial education and creating the most optimal financial plans for their clients.