By: Liz Strait, PhD

Introduction

Most Americans use some form of financing to purchase a new vehicle—a full 84% of new car purchases entailed financing in 2022.1 As a Financial Professional (FP) it is important to monitor borrowing costs given that the vast majority of US consumers borrow to buy a new vehicle. In the past year, these costs have increased dramatically—almost one in six borrowers now have a monthly payment in excess of $1,000; average interest rates are at the highest level they have been in over a decade; and average loan terms are lengthening to between six and seven years. This has led to an increasing rate of delinquency and repossession. Even clients with good loans or without loans are at risk should default rates increase—more defaults can lead to a potential credit crunch as cash flow is reduced at the financial institutions holding these loans.

Background

The average amount paid for a new car in the US was $48,008 as of March 2023.2 This compares to $36,824 in 2021.3 While some of this increase is due to increasing prices from supply shortages4, it is also for another (important) reason—more Americans are buying luxury cars. The share of new car sales that were luxury vehicles was 19.5% in February 2023.5 Compare that to approximately 15% at the end of 2020 and just under 13% at the end of 2012.6 With an average sticker price of about $64,4004, this means an increasing number of new car buyers are spending more on their cars.

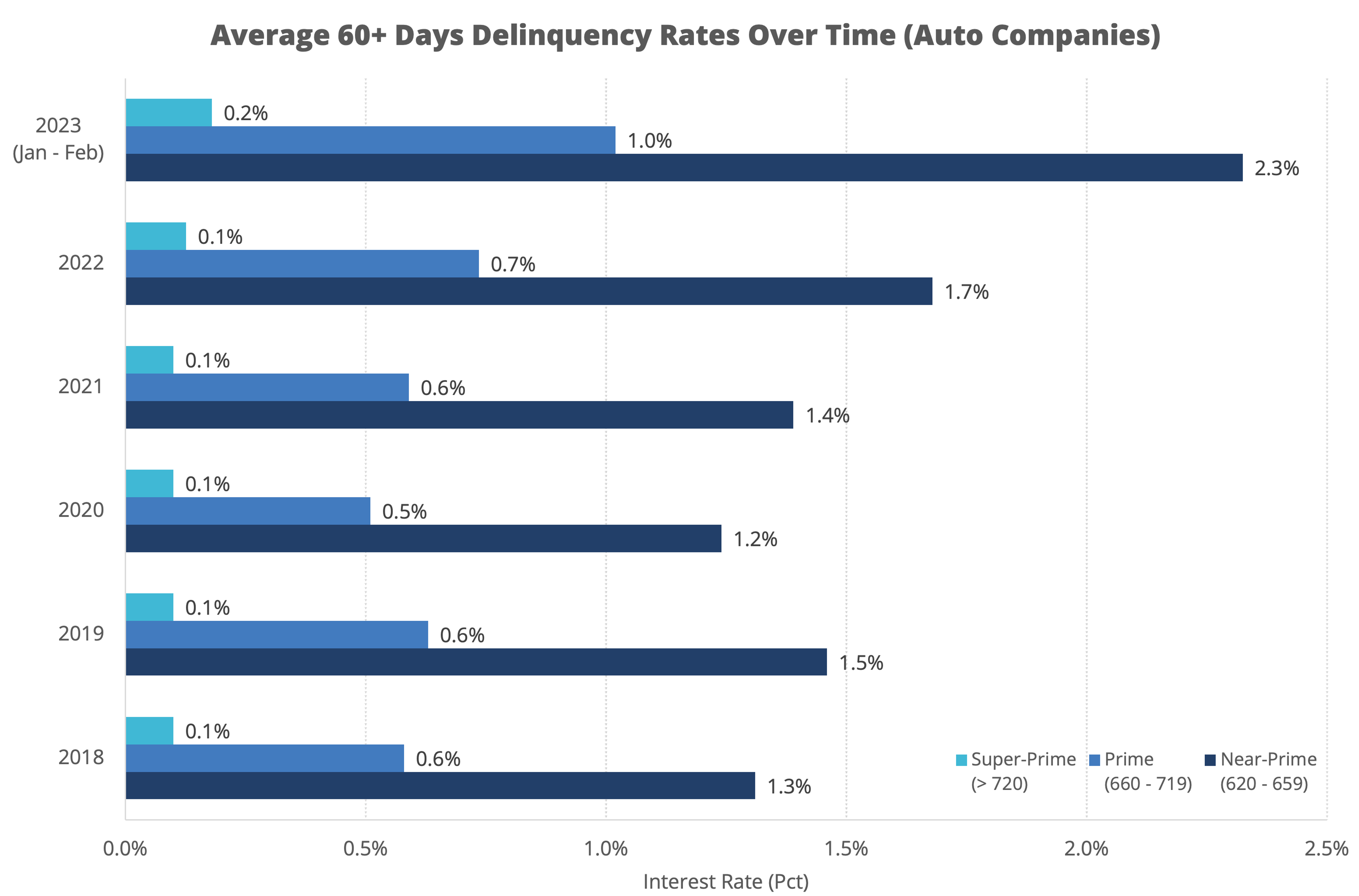

But why is this problematic? There are several reasons. First, the average price paid for a luxury car has increased 9.2% since July 2019 and 8.7% since July 2020.7 However, the median household income has decreased by 3.4% since 2019 and by 1.2% since 2020.8 This means, on average, Americans are spending a greater proportion of their annual income on their cars. And that doesn’t include the increased cost of borrowing. Average loan rates are at a 15-year high, with new car financing rates at 7.1% as of June 2023, resulting in an average monthly payment of $733 (also a record high).9 A monthly payment of $733 is 17% of the average American household’s monthly income after taxes.10 Finance experts suggest paying no more than 10% of your monthly income on your car payment—meaning many US households are in a financially risky position.11 Speaking to this, delinquency rates (of 60+ days) have increased to 0.5% as of February 2023 (compared to 0.3% in 2018) for consumers with a prime or super-prime credit scores (scores 660+).12 Across credit ratings, delinquency rates are 26.7% higher now than they were a year ago.13

Another concerning statistic is that over 17% of consumers have committed to monthly car payments of $1,000 or more.9 Consumers with these extremely high payments fall into two groups. The first group is less problematic and far smaller—these are consumers who signed up for significantly shorter loan terms at significantly lower APRs, accepting higher monthly payments to reduce the total interest paid. The second group, which is 65% of consumers who signed up for $1,000+ monthly payments in 2023, have an average loan term ranging between 6-7 years and an average interest rate of 9.6%.9 These consumers will end up paying thousands of dollars towards interest alone. And this trend is not isolated to the first half of 2023—30% of the current auto loan market is long-term loans and only 5% are paid off in 2-3 years.14

We may also see further problems for consumers because of the falling price of used cars. According to Cox Automotive, the average price of a used car has decreased 13.1% from the start of 2022.15 As cars lose value over time, especially if they are losing that value more quickly, many car owners end up upside down on their auto loans (i.e., the value of their vehicle is less than what they owe on the loan). Even car owners with good loans or without loans at all are affected by falling used car prices—this lowers the value of all cars and, therefore, the value of total equity held.

Even buyers with good loans or without loans are at risk should default rates increase—more defaults can lead to a potential credit crunch as cash flow is reduced at the financial institutions holding these loans.

As the cost of new cars increases in conjunction with the increased cost of borrowing (higher interest rates), more Americans have negative equity in their cars. Negative equity in and of itself isn’t unusual, as the value of new cars depreciates quickly, but the level of negative equity has increased since 2021—the percentage of new car sales with a trade-in that had negative equity rose from 14.9 to 17.4 from 2021 to 2022.14 This means that when consumers go in to buy a new car, they can end up rolling over debt from their old car (i.e., the trade-in value or private sale price for a car is less than what the individual owes on their existing loan). In other words, consumers can leave a dealership with a loan on a new car that far exceeds the value of that new car, which only increases negative equity further. Increasing negative equity also reduces consumers’ options for refinancing or selling their car to alleviate debt. Borrowers with higher negative equity are more likely to go delinquent and/or default on their auto loans. This could lead to a credit crunch and possible credit crisis as cash flow is reduced at financial institutions holding these loans, which affects all consumers—not just those with bad auto loans.

The takeaway from much of this is there is a significant sub-population of consumers who are choosing objectively bad loans—loans resulting in negative equity, significant and unsustainable interest payments, and ridiculously long term-lengths. Part of this is unavoidable and due to a more recent development: the removal of loan options for low-credit consumers and the elimination of low-MSRP vehicles. To illustrate, Kelley Blue Book points out that deep subprime loans (those to consumers with the lowest credit scores) are effectively nonexistent at this point.14 Even subprime loan availability has dropped significantly—in March 2020, subprime loans comprised 15% of the market, by December 2022, this share had dropped to about 5%.16 With these borrowers priced out of the market17, automobile manufacturers have started focusing on the most profitable vehicle models18—those targeted at consumers who can afford to buy, which perpetuates the unavailability of funds to buyers with low credit. This will have ramifications for years to come as the price of used cars remain too high for those consumers with deep subprime and subprime credit scores.

But the second contributor to the existence of bad loans is buyers making bad borrowing decisions. This problem affects consumers in all credit categories, not just those in the lower credit score tiers. The average interest rate for new vehicles varies greatly depending on the source of the funds. While the common advice to all car buyers is “shop around,” most consumers do not—80% of auto loans are brokered through dealers.19 Further, many consumers do not realize that lower monthly payments usually come with higher APRs and, thus, much higher total interest payments. For example, the life-of-loan savings for even a super-prime borrower can be almost $2,000 if they shop around for auto loans.20 Choosing bad loan terms can put a buyer in financial jeopardy—both as their budget may be stretched tighter and unable to accommodate unexpected expenses, and in terms of opportunity costs. As consumers pay more for longer, they aren’t using that money for more productive purposes (i.e., savings, 401k contributions, down payments on a house, etc.).

End Notes

[1] “Share of Used and New Cars Financed in the U.S. 2017-2022.” Statista, 2023, https://www.statista.com/statistics/453000/share-of-new-vehicles-with-financing-usa/.

[2] Tucker, Sean. “Average New Car Price Falls Below Sticker for First Time in Almost 2Years.” Kelley Blue Book, 13 Apr 2023, https://www.kbb.com/car-news/average-new-car-price-falls-below-sticker-for-first-time-in-almost-2-years/.

Entering 2023, the average price was over $49,500 (see 1).

[3] Meyer, Susan. “Average Car Price is at an All-Time High of $47,000 Going into 2022.” The Zebra, 28 Mar 2023, https://www.thezebra.com/resources/driving/average-car-price/.

[4] Tucker, Sean. “A Train Car Shortage is Keeping Vehicles Out of Dealerships.” Kelley Blue Book, 19 Jun 2023, https://www.kbb.com/car-news/a-train-car-shortage-is-keeping-vehicles-out-of-dealerships/.

During the COVID-19 pandemic there was a shortage of semiconductor chips used in new cars, which led to fewer new cars being built to completion and a decrease in new car supply. Just as those supply chain issues were resolved, a new restriction on supply has arisen: transportation shortages (i.e., there aren’t enough railcars to ferry new cars from production to dealerships). This means that new car prices are increasing, since there are more cars desired than available. Until recently, car buyers followed a general rule of thumb—never pay sticker price—now, we see new cars being purchased above MSRP. For example, as of Q4 2022, Hyundai and Kia were selling most of their cars at 5-6% above sticker price.

The increased demand for luxury cars represents a change in tastes—this will drive up average car prices regardless of supply fluctuations, suggesting there will be a continued upward trend in new vehicle prices.

[5] As of May 2023. See: Tucker, Sean. “Average New Car Price Holding Steady Under Sticker.” Kelley Blue Book,12 Jun 2023, https://www.kbb.com/car-news/average-new-car-price-holding-steady-under-sticker/.

February 2023 saw the peak share for luxury cars, but the share has been approximately 19% for all of 2023 so far.

[6] Tucker, Sean. “Americans Keep Buying More Luxury Cars.” Kelley Blue Book, 3 Nov 2022, https://www.kbb.com/car-news/americans-keep-buying-more-luxury-cars/.

[7] Percent change calculated based on historical price data from “Average New-Vehicle Prices Up 2% Year-Over-Year in July 2020, according to Kelley Blue Book.” PR Newswire: Press Release Distribution, Targeting, Monitoring and Marketing, 3 Aug 2020, https://www.prnewswire.com/news-releases/average-new-vehicle-prices-up-2-year-over-year-in-july-2020-according-to-kelley-blue-book-301104310.html.

[8] Median household income was $72,808 in 2019 and $71,186 (both in 2021 adjusted dollars) according to the Federal Reserve Economic Data, accessible here: “Real Median Household Income in the United States (St. Louis Fed).” Federal Reserve Economic Data (FRED), https://fred.stlouisfed.org/series/MEHOINUSA672N.

Median household income is estimated to be $70,333 for January 2023 in 2021 adjusted dollars (amount adjusted using U.S. Bureau of Labor Statistics CPI Inflation Calculator, accessible here: https://www.bls.gov/data/inflation_calculator.htm).

The estimate for January 2023 median household income comes from: “Median Household Income in January 2023." Seeking Alpha, 1 Mar 2023, https://seekingalpha.com/article/4583302-median-household-income-in-january-2023.

[9] James,Talia, and Paul Mitchell. “Car Shoppers Feel the Heat from Scorching Financing Costs in Q2, according to Edmunds.” Edmunds, 3 Jul 2023, https://www.edmunds.com/industry/press/car-shoppers-feel-the-heatfrom-scorching-financing-costs-in-q2-according-to-edmunds.html.

[10] Average take-home income found here: https://stats.oecd.org/index.aspx?queryid=55145 and adjusted to 2023 dollars using the U.S. Bureau of Labor Statistics CPI Inflation Calculator (see [8]).

[11] Bradley, Shannon. “How Much Should My Car Payment Be?” NerdWallet, 14 Jun 2016, https://www.nerdwallet.com/article/loans/auto-loans/much-car-payment.

[12] June 2023 Credit Union Auto Lending Market Report, accessible here: https://www.cuna.org/content/dam/cuna/advocacy/cu-economics-and-data/data---statistics/auto-lending-monthly-report/ALMR_0423%20(2).pdf

This rate is even worse for consumers with near-prime credit scores (620 – 659): the current delinquency rate is 1.9%, compared to 1.2% in 2018.

[13] “AutoMarket Weekly Summary: January 13.” Cox Automotive Inc., https://www.coxautoinc.com/market-insights/auto-market-weekly-summary-january-13/.

[14] Tucker, Sean. “New Cars Were Easier to Afford in March.” Kelley Blue Book, 17 Apr 2023, https://www.kbb.com/car-news/new-cars-were-easier-to-afford-in-march/.

[15] “Manheim Forecast: Used-Vehicle Values Expected to Normalize in 2023 After Record Volatility.” Cox Automotive Inc., https://www.coxautoinc.com/news/manheim-forecast-used-vehicle-values-expected-to-normalize-in-2023-after-record-volatility/.

This is the unadjusted price difference.

[16] Hickey, Christopher. “Car Loan Interest Rates Are Reaching Record Highs and Taking Longer than Ever to Pay off.” CNN, 15 Apr 2023, https://www.cnn.com/2023/04/15/cars/car-loan-interest-rates-2023-dg/index.html.

[17] Tucker, Sean. “Car Shoppers With Lower Credit Scores Increasingly Have Nowhere to Go.” Kelley Blue Book, 8 May 2023, https://www.kbb.com/car-news/car-shoppers-with-lower-credit-scores-increasingly-have-nowhere-to-go/.

For buyers with super-prime credit, a 72-month loan with 10% down on a $48,000 car would receive an interest rate of 6.2%, that would result in a monthly payment of $720. This exact same loan for the exact same car would result in a rate of 17.9% and a monthly payment of $983 for a subprime buyer. This looks even worse by the end of the loan—the high-credit buyer will have paid $8,700 in interest. The subprime buyer? $27,000.

[18] Many automobile makers have eliminated their cheapest models—subcompact cars. In fact, with both Chevrolet and Hyundai dropping their subcompact lines, there are only three subcompact cars left on the market. The cheapest vehicle now available is the 2023 Nissan Versa, which starts at $15,730. As of 2023, there are only 10 cars on the market with MSRP’s below $25,000. In 2018, there were 36.

See: Tucker, Sean. “2023 Nissan Versa Takes Cheapest New Car Title.” Kelley Blue Book, 15 Nov 2022, https://www.kbb.com/car-news/2023-nissan-versa-takes-cheapest-new-car-title/.

Tucker, Sean. “Already Tight, Auto Loan Standards Tightened in May.” Kelley Blue Book, 9 Jun 2023, https://www.kbb.com/car-news/already-tight-auto-loan-standards-tightened-in-may/.

[19] Felton, Ryan. “The Big Business of Bad Car Loans.” Consumer Reports, 22 Jan 2022, https://www.consumerreports.org/money/car-financing/the-big-business-of-bad-car-loans-a2181686536/.

[20] This is assuming a 72-month loan term with $40,000 being financed. The savings is for the lowest average APR offered to super-prime customers on such a loan versus the highest APR offered to the same group of consumers on such a loan. See [12] for more information.